A question that many people have on their minds is how much insurance should I get on my car? The answer to this will depend on your needs and what you can afford. For example, if you are a student who has just started working and needs to commute or someone who still lives with their parents, then it might be best for you to get the minimum coverage. If you live in an area where there are high crime rates, then it might be wise for you to purchase higher levels of coverage so that anything unfortunate does not happen. You never know when something could happen that would make things difficult financially and having extra protection could help out a lot in those situations.

When you are looking at getting auto insurance, there are different factors that can affect the price. These include where you live, what type of car it is, and how old you are. Each factor will determine whether a person is required to have extra coverage on their policy and what kind of rates they will pay for it. A good example of what factors will affect the price of your insurance is to look at teenagers. The reason why teenagers are charged more for auto insurance than adults is that they make many mistakes when they first get their license and do not have enough experience driving. Also, most of them tend to speed which makes it a lot riskier for companies to insure these young drivers.

When it comes to what insurance you should get, it all depends on your situation. If you just moved to an area where there are more accidents then chances are that insurance will be a lot more expensive than in other areas. Also, if you live near the city or right outside of the city, then getting added coverage for theft might not be a bad idea because there are more chances that your car could be stolen. You will also want to make sure to check the types of cars you will need insurance for, especially if you have several cars in the garage. All of these factors can increase your insurance rates and there is no way around it.

If you happen to live in an area that has a lot of crime rates then you might want to consider getting theft insurance if you do not have anything stolen. The prices for this type of coverage may be much higher but it will be worth it in the long run. Plus, some people like to get multiple cars insured with one agency so they can take advantage of discounts offered by the agency.

Another thing to consider is the type of car that you have because this can also increase your insurance costs. If you have a sports, semi-exotic, or exotic car then chances are that it will be more expensive to insure than other types of cars on the road. These types of cars tend to get into more accidents and they have a higher theft rate which is the reason why they cost more.

If you are looking for affordable insurance, then you should take a look at carpooling, public transportation or taking the bus instead of driving your own car. These options might seem inconvenient but in the long run it can save money and be safer for everyone on the road.

Here are some guidelines to follow when finding your insurance company.

A. Determine the cost of your car

The first step in getting an insurance quote is to figure out what your car is worth, because that's going to weigh heavily on how much coverage you need. The only way to find out what your vehicle is worth on the open market is by researching current private party sale prices for similar vehicles in your area. You can find that information in the classifieds section of your local newspaper or online via a number of sites, including AutoTrader.com and AutotraderClassics.com.

You should list all the important features of your car like miles per gallon, whether it is 4x4 or not, automatic or manual transmission, the make year and model, whether it is a convertible or hard-top/Convertible, if its in pristine condition, or just average. You have to research how much similar vehicles are selling for and add about 5% to 10% for the dealer profit markup (i.e. what they expect to get from you). The reason to add 5–10% for the dealer's profit is because they pay to advertise and a listing fee.

With this information, you can get an idea of what kind of coverage you should be looking to purchase in terms of liability limits. Depending on how much your car is worth, $100,000/$300,000/$500,000 or even higher may be needed.

Once you know how much coverage you will need, the process of getting your insurance quote will get easier.

B. Get an auto insurance quote online or call a broker

The next step in figuring out how much auto insurance to buy is to shop around on the web for a quote or call a local independent insurance agent or broker. An automotive insurance broker can help you compare rates at multiple companies in an instant, and that's a time-saver no matter what.

The website of the Insurance Information Institute has some tips on the home page to get you started:

• Get quotes from at least three different insurers to find out which one is offering the best deal for you.

• Ask about discounts. Some discounts include good driver, multiple-car and loyal customer (for staying with one company for at least five years).

• If you are comparing policies from different companies, be sure to read the fine print carefully to make sure each policy offers the same coverage.

• Make sure your provider will cover you if you are in a multiple-vehicle accident or an accident with a driver who does not carry adequate insurance.

• Make sure the insurer's policy complies with state laws (see Nolo's article on choosing a car insurance company.) You can also check with the National Association of Insurance Commissioners ( www.naic.org ) to see if your provider's rates are in line with other insurers for the same type and level of coverage you're considering.

DISCUSSION QUESTIONS:

(1) What is a deductible? Why would you want one? How does it affect insurance premiums?

(2) How is insurance usually priced? Why are different companies offering you more or less coverage?

(3) What should you do about a quote that is too high? About one that is too low?

C. Comparing insurance rates on the web

If you have taken these steps and shopped around for an auto insurance quote, chances are you will have discovered that different companies offer widely varying rates, even for the same level of coverage. For instance, one company can be offering $440/year for 6 months, and then another could give you a quote of $600/year or more.

Since an insurance premium is simply the amount of money the insurer is guaranteeing to pay for your losses, it is important to understand how insurance pricing works in order to evaluate the cost/value of an offer you may get from a particular company.

One thing that reduces your risk of accidents and damage is discounts. These are some common ones:

• Tinted windows (reflects the sun's heat as opposed to absorbing).

• Multiple-car (lower your risk of losing the only car you have).

• Good student (have a good GPA get some college credit)

• Driver training courses (to improve driving skills).

• Young, healthy driver or mature driver.

• Discounts for not driving a lot. If you are going to be at home most of the time, why buy a lot of coverage?

• Low mileage drivers (if you drive very little).

• Homeowners insurance discounts (auto policy purchased paid for with the same insurer).

• Mature driver discounts - not many companies offer this but it is worth looking into. A mature driver is someone who does not just have experience, but also has the personality and emotional maturity to handle the driving task well.

• Multi-policy discounts - if you have two or more policies with the same insurer, they might give you a discount for being such a loyal customer.

• Collision and comprehensive coverage on your car - in other words, if it is stolen or damaged totaled, the insurance should pay enough so that you can purchase a new one without having to pay anything out of pocket (non-totaled).

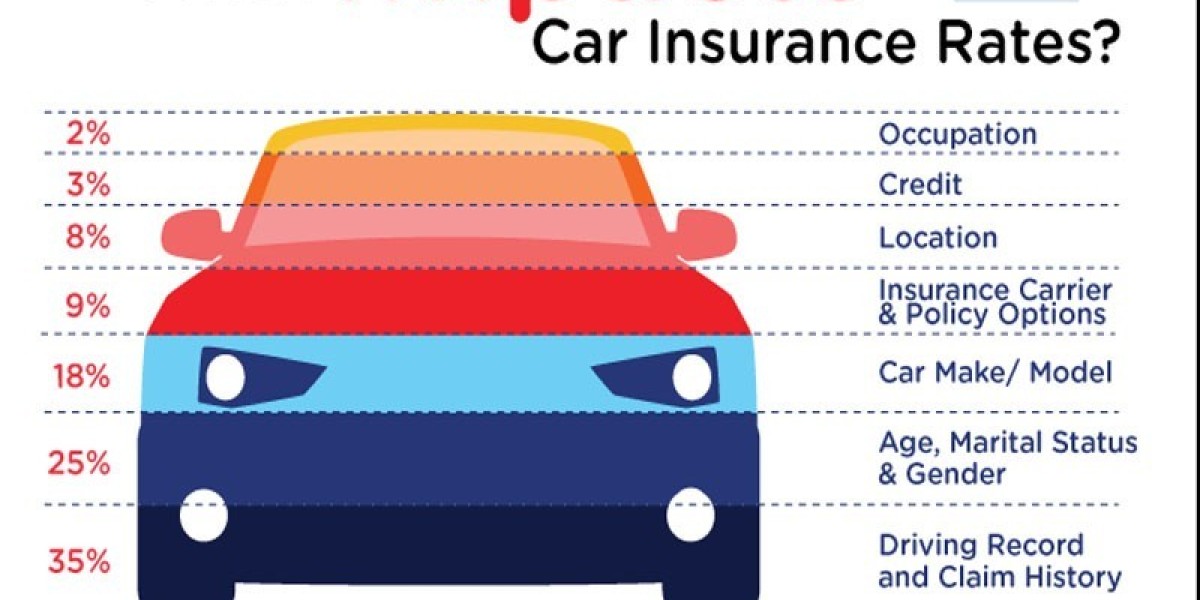

The first thing an insurance company looks at is your driving record. It is not enough that you take defensive driving courses because these do not make much difference in determining what your premium will be. You must have a clean record for several years and be able to show proof that your record is clean.

Another factor in determining how much you will pay for auto insurance is where you live and drive. Rates vary from state to state and within the same state from city to city. City drivers tend to have more accidents so their premiums are higher than those of someone who lives in a rural area.

The factors that play a big role in your premium are:

• Age and driving record.

• Number of miles driven per year.

• Type and size of vehicle(s) you drive(d).

• Marital status (single, married, divorced or widower), age number of dependents (usually not relevant for teens as they will not be supporting a family).

• Credit score.

• Your insurer – a company that has been around for longer will have more experience with handling claims and settling them appropriately and efficiently.

The best way to compare auto insurance quotes is by visiting the websites of at least three providers in your state and looking at their rates. Some people like to compare rates and coverages using a local agent, but many are not as knowledgeable about the intricacies of insurance law and can't shop for you to get you the best deal. So it is more efficient and economical to look at quotes from online providers who have already done much of the legwork in finding you rate quotes.

As long as your auto insurance is valid, your car will be covered for loss or damage due to weather conditions, fire, theft, or vandalism. If you are involved in an accident and it is not your fault, your policy should help with the cost of repairing/replacing damaged/stolen property and medical expenses related to injuries incurred during the accident.

If you have comprehensive and collision coverage, you must submit the claim to your insurance provider to be reimbursed for damage done to your vehicle. If you don't have these coverages, it is vital that you save all receipts related to loss or damage so that you can apply for reimbursement later on. You might also consider taking photos of the damages as well as the property to be sure that your claim is processed smoothly.

In a nutshell, the more insurance coverage you have on your car, the higher premium you will pay (to an extent). If you have no or low coverage and you get into an accident, it might mean going into debt in order to repair/replace your vehicle before being able to drive again.

Fully comprehensive car insurance, on the other hand, is expensive and not necessary for every driver since most drivers don't need to pay a high deductible out-of-pocket cost should they get into an accident. However, if you tend to be in accidents more often than others or can't afford to pay $1000 out of pocket as a deductible, you might want to consider buying more comprehensive insurance since it will protect you from paying out of pocket should you get into an accident.

One thing to keep in mind is that when looking at your auto insurance quote, don't just look at the premium price – also take a look at the coverage and any add-ons or extras the insurance provider is offering you. This will help you make a more informed decision and avoid buying insurance that you don't need or will waste money on.